EMI Calculator

Your Amortization Details

+| Year | Principal (A) | Interest (B) | Total (A+B) | Balance |

|---|

Introduction: Let’s Talk About the Elephant in the Room

Let’s be honest with each other. Nobody wakes up in the morning and says – “I want a loan today.”

What we really want is the house, the keys to that new Mahindra Scorpio N, the look of new Thar or the thumping sound of the Royal Enfield Classic 350 that we have been ogling for last one year. We want to pay for that dream wedding or to solve a medical emergency without breaking. The loan? That is just a heavy burden we must bear to get to the destination.

But here is the problem: Taking a loan is terrifying.

I remember entering a bank – air-conditioned working environment, polite staff, coffee for free – and was hit with such words as “reducing balance,” “repo-linked rates,” “amortization schedules,” and “tenure adjustments.“. I became confused. I just nodded, put my signatures on the papers and walked out feeling strangely lightheaded and got a tea from a street vendor.

It is only three years down the road, when dust is in the air and one looks at their bank statement. The panic sets in – those EMIs have consumed lakhs of rupees, but my principal amount owed has barely budged. I start wondering: “How much of my salary is actually going to vanish every month for the rest of my life?”

I believe that is the case of most of you.

That is exactly why I built CalcSahayak.

I didn’t want just another basic online calculator that spits out numbers. I wanted to build a comprehensive loan calculator that serves as your Sahayak (Ally) in this financial battle. I wanted to build a resource that shows you the truth about your money without complicated financial terms. Whether you want to find the down payment on a 3BHK flat or to calculate the “Total Interest” for a second-hand car through our software, both this guide and the tool will show you where every rupee goes.

This isn’t just a calculator page. This is a 3,000-word deep dive into the mechanics of debt. I am going to cover everything from the “Golden Triangle” of lending to the specific Excel formulas you can use. This guide will help you to understand how EMI operates, how a debt can be paid earlier, how much loan you should get, and much more.

Grab a coffee. We have some money to save.

Part 1: What Actually Is an EMI? (It’s Not Just a Payment)

EMI stands for Equated Monthly Installment. It is the fixed amount (not variable) that leaves your bank account on the 5th or 10th of every month usually.

But if you look under the hood, an EMI isn’t one thing. It’s two enemies fighting for space in your wallet.

- The Principal: This is the good part. This is you actually paying back the money that you borrowed. Every rupee that goes here increases your ownership of the asset.

- The Interest: This is the “rent” you pay for using the bank’s money. This money is gone. Poof. Vanished.

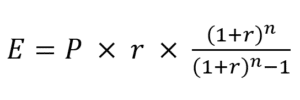

What They Use In The Formula. The “Secret” Math.

If you want to check the numbers yourself (or impress your bank manager), this is the exact formula used by every major Indian bank (SBI, HDFC, ICICI, etc.)

Where:

- E = EMI

- P = Principal (Loan Amount)

- r = Monthly Interest Rate (Annual Rate ÷ 12 ÷ 100)

- n = Loan Tenure in Months

The “Front-Loading” Trick

Here is the part that shocks most borrowers the first time around. Banks use this formula to maximize their profits.

If you use the CalcSahayak Tool above and click on the “Amortization Schedule,” look at the breakdown for Year 1 of a Home Loan.

- 70% to 80% of your monthly payment is the Interest.

- Only 20% to 30% goes towards the Principal.

This is why, if you try to close a 20-year loan after 5 years, you are often horrified to find you still owe practically the full original amount. You haven’t been paying off the loan; you’ve been paying the interest on it.

Knowing this doesn’t mean you shouldn’t take out the loan. It means you need a plan to flip those percentages as soon as possible.

Part 2: The Cheat Sheet – Popular EMI Lookup Tables

I know probably nobody is here to read a thesis. Some of you are standing in a car dealership or sitting in a bank lobby right now. You need a number and that’s all.

I’ve done to death the accounting on the most common Indian loan situations. Find your bracket below.

🏠 Home Loan EMI Calculator

Before you commit to a 20-year debt, run the numbers through a proper home loan EMI calculator. Below is a cheat sheet based on standard market rates (assuming interest rate @ 8.5%).

Loan Amt |

15Y EMI |

20Y EMI |

25Y EMI |

Total Int 20Y |

|---|---|---|---|---|

₹20L | ₹19,695 | ₹17,356 | ₹16,105 | ₹21.6L |

₹ 30L | ₹29,542 | ₹26,035 | ₹24,156 | ₹32.5L |

₹ 50L | ₹49,237 | ₹43,391 | ₹40,261 | ₹54.1L |

₹ 75L | ₹73,855 | ₹65,087 | ₹60,392 | ₹81.2L |

₹ 1Cr. | ₹98,474 | ₹86,782 | ₹80,523 | ₹1.08 Cr. |

💡 The CalcSahayak Insight: Check out the ₹50 Lakh row. Your EMI only drops down by ₹3,000 if you extend your loan from 20 to 25 years. But in the end, you pay lakhs more in interest. Always choose the shortest term that you can afford.

💰 Personal Loan EMI Calculator & Lookup Table

Assumption: Interest Rate @ 11.00% (Typical for salaried employees)

Loan Amt |

1 Yr |

3 Yrs |

5 Yrs |

|---|---|---|---|

₹1L | ₹8,838 | ₹3,274 | ₹2,174 |

₹3L | ₹26,514 | ₹9,822 | ₹6,523 |

₹5L | ₹44,191 | ₹16,369 | ₹10,871 |

₹10L | ₹88,382 | ₹32,739 | ₹21,742 |

🚗 Car Loan EMI Calculator & Quick-Reference

Assumption: Interest Rate @ 9.00% (New Car)

Loan Amt |

3 Yrs |

5 Yrs |

7 Yrs |

|---|---|---|---|

₹5L (Swift) | ₹15,900 | ₹10,379 | ₹8,045 |

₹10L (Nexon) | ₹31,800 | ₹20,758 | ₹16,089 |

₹20L (XUV700) | ₹63,599 | ₹41,517 | ₹32,178 |

Part 3: How to Use This Loan EMI Calculator (Without Getting Confused)

I designed the CalcSahayak interface to be clean, but garbage in equals garbage out. Here is how to set the sliders correctly.

1. The Loan Amount (Principal)

Mistake to Avoid: Do not put the price of the house or car here. If you are buying a flat for ₹60 Lakhs, then your bank isn’t lending ₹60 Lakhs. You are required to make a down payment (which is usually 10% – 20%).

✅ Correct Input: ₹60 Lakhs – ₹12 Lakhs (Down Payment) = ₹48 Lakhs.

2. The Interest Rate

This is where the magic happens.

🏠 Home Loans: Currently floating between 8.35% and 9.5%.

🚗 Car Loans (New): 8.75% to 11%.

⚠️ Used Car Loans: 12% to 18% (Be very careful here).

💰 Personal Loans: 10.5% to 24%.

3. The Tenure

This slider controls your monthly budget.

Short Tenure = High EMI, Low Total Interest (Smart Choice).

Long Tenure = Low EMI, High Total Interest (Convenient Choice).

4. The "Doughnut of Truth"

Once you hit calculate, look at the circle chart.

🟢 Green Slice: Interest.

🔵 Blue Slice: Principal.

If the Green slice is larger than the Blue slice (common in long-term home loans), you are paying back more than double what you borrowed.

Part 4: A Strategic Playbook by Loan Type

One size does not fit all. Calculating EMI for a smartphone is very different from calculating it for a House. Here is your niche-specific strategy.

🚗 Car Loan Strategy: The "Depreciation Trap"

Whether you are buying a Maruti Swift, a Tata Nexon, or a luxury BMW, cars have one thing in common: They lose value every day.

The 5-Year Rule:

Never, ever take a car loan for longer than 60 months (5 years).

Why? Because by year 6 or 7, the car’s market value will likely be lower than the amount you still owe the bank. This is called being “underwater” on a loan; you don’t want to be paying EMI on a car which already rattles and is out of warranty!

The “Used Car” Warning:

If you are purchasing a second-hand vehicle, look out for lenders who accept interest rates of 14% to 16%. Use the calculator to compare:

- New Car @ 9% for ₹10 Lakhs.

- Used Car @ 15% for ₹8 Lakhs.

You may find the overall monthly outflow is not greatly different.

🏠 Home Loan Strategy: The "Marathon"

This is the big one. 20 to 30 years of commitment.

The 40% Rule:

Your Home Loan EMI should ideally not exceed 40% of your monthly take-home pay. If you push it up to 50% or 60%, then there’s no provision for emergencies, vacations, or investment opportunities. You become “House Poor” — living in a big house without a rupee in your pocket.

The Prepayment Hack:

As Home Loans are such huge amounts, small changes have big impacts. If you pay just one extra EMI per year, you can reduce roughly 3 to 4 years off your total tenure.

- Yes, you read that correctly. Just one more annual payment removes 4 years of debt.

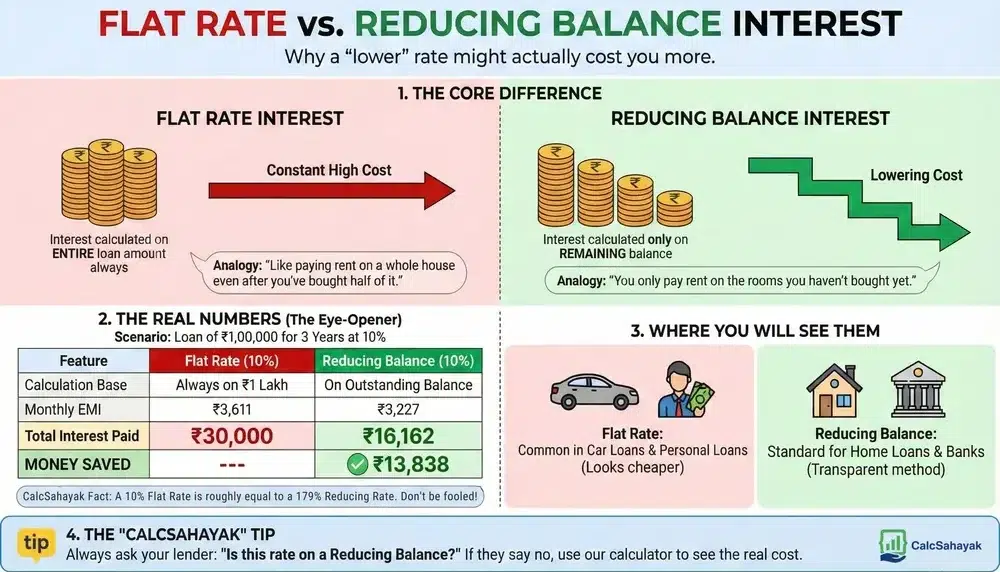

🏍️ Bike Loan Strategy: The "Flat Rate" Trick

If you were buying a Royal Enfield Classic 350 or a Honda Activa at a dealer, he might say this: “Sir, we have a special interest rate of just 4%!”

Stop!

Ask him: “Is that a Flat Rate or Reducing Balance?”

- Reducing Balance (Good): Interest is charged only on outstanding amount.

- Flat Rate (Bad): Interest is charged on the original full loan amount for the entire tenure, even as you pay it back.

The Flat Rate of 4% over 3 years is almost equal to a Reducing Balance rate of 7.5% to 8%. So don’t be fooled by that small number – use our calculator to work backward from the EMI he quotes to find the real interest rate (or IRR).

📱 Gadgets & Personal Loans: The "No Cost" Myth

Try on Amazon and Flipkart: “No Cost EMI on iPhone 17 pro.”

Is it really free? Most times, the answer is no.

Two of the ways they often do this is to offer:

- Discount Forfeiture: If you paid cash, you might get a ₹5,000 instant discount. By taking “No Cost EMI,” you lose that discount. That ₹5,000 is your interest.

- Hidden Interest: The interest is built into the price of the product.

The CalcSahayak Insight: Always calculate – (EMI Amount x Number of Months). Compare that to the price of the product at a local offline store.

Part 5: For the Data Geeks – How to Calculate EMI in Excel

Maybe you don’t trust the web tools. While a compound interest calculator helps you grow wealth, this sheet helps you stop losing it. Maybe you simply want to build your own financial dashboard. I appreciate this. Transparency is our core value here. Let’s get started.

No need for complicated macros. All you need is the PMT function.

Step-by-Step Guide

Open a blank sheet in Excel or Google Sheets.

Cell A1 (Rate): Type your annual interest rate here (e.g.,

8.5%).Cell A2 (Months): Type the number of months (e.g.,

240for 20 years).Cell A3 (Loan Amount): Type the loan amount.

⚠️ CAUTION: Put a minus sign in front of it (e.g.,

-5000000).

Cell A4 (The Result): Type this formula:

= PMT (A1/12, A2, A3)

Why divide by 12? The rate in A1 is an annual rate, but you pay monthly. Dividing by 12 converts it to a monthly interest factor.

💡 Don’t want to bother typing?

Includes a full Amortization Table, Prepayment Calculator, Print ready version, and much more.

— OR UPGRADE TO PREMIUM —

The "Offline"

Privacy Vault

Banker-Grade Precision. 100% Offline.

- No Spam Calls: Data stays on your laptop. No tracking.

- Diwali Bonus Ready: Add irregular prepayments & see magic.

- Tax Ready: April-March breakdown for your CA.

One-time purchase. Lifetime Access. Secure Offline File.

Part 6: The "Golden Triangle" of Loans

Every loan is a three-sided triangle. If you change one side, the other two must shift.

- Principal (Amount)

- Tenure (Time)

- EMI (Payment)

(Interest Rate is the environment you live in; you can’t control it as much, but you can negotiate it.)

The Tenure Trap (Read This Before Signing)

Most people try to minimize the EMI side of the triangle by stretching the Tenure side. It is lighter on the pocket.

“Let’s make it 25 years instead of 20” they say hypothetically.

Let us take the maths of a ₹50 Lakh Loan @ 8.5%:

- Scenario A (20 Years):

- EMI: ₹43,391

- Total Interest Paid: ₹54 Lakhs

- Scenario B (25 Years):

- EMI: ₹40,261

- Total Interest Paid: ₹70 Lakhs ❌

The Analysis:

By stretching out the loan, you saved ₹3,130 per month.

But over the life of your loan, you paid the bank an extra ₹16,00,000!

Is saving ₹3k a month worth throwing away the price of a brand-new Mahindra Thar in interest? Typically, the answer is no.

Part 7: Five Levers to Lower Your EMI

If the calculator tells you the quantity and the mere thought of it scares you, you may as well give up. Right? Don’t worry. There are levers you can pull to change that.

1. The "Down Payment" Lever

Every rupee you pay up front is a rupee you don’t have to pay interest for 20 years.

- Strategy: If you are buying a car, sell your old car privately (OLX/Spinny) rather than trading it at the dealership. You will surely get 10-15% more cash, that you can use as the down payment.

2. The "Step-Up" Lever

Some banks (SBI, HDFC, etc.) offer “Step-Up” loans.

- How it works: You pay a lower EMI for the first 3-5 years (when you are young and your salary is lower). The EMI gradually increases as you get promoted.

- Who it’s for: Young professionals who need a boost in eligibility now but expect salary hikes later.

3. The "CIBIL" Lever

Your credit score isn’t just a number on people’s lips. You can use it as negotiation tool.

- 750+ Score: You qualify for the “Risk Premium” discount. You can demand the lowest advertised rate.

- Below 700: You will be charged a “spread” (extra interest).

- Strategy: Before applying for a large Home Loan, take 6 months to fix your score. Pay off small credit card bills, don’t apply for random loans. A 0.5% interest difference saves lakhs.

4. The "Balance Transfer" Lever

Are you still living with the 10% loan from five years ago?

- Find out where the market is at: If current rates are 8.5%, you are losing money.

- The Move: Use our calculator to work out the potential saving. If this is more than the processing fee (usually 0.5%), move your loan to a new bank.

5. The "Prepayment" Lever (The Holy Grail)

This is how you beat the bank.

Most floating rate home loans have no penalty for prepayment.

- Diwali bonus? Throw it into the loan.

- Tax refund? Throw it into the loan.

- Uncle gave you some money? Throw it into the loan.

Even a small prepayment attacks the Principal directly, bypassing the interest component entirely.

Part 8: Frequently Asked Questions (FAQ)

We scanned the search queries (and our emails) to find the most common questions you are asking.

Q: Can my EMI change during the loan?

A: Yes and No.

- Fixed Rate Loan: No. Your EMI stays the same forever (Home Loans are different, but for Car/Personal Loans this is typical).

- Floating Rate Loan: Yes. If the RBI changes the Repo Rate, your bank changes your rate.

- Note: Banks usually increase your Tenure (number of months) not your EMI amount to keep your monthly budget stable. You might be paying for 25 years instead of 20 without even realizing it. Check those statements!

Q: Does this calculator include Processing Fees and GST?

A: This tool calculates the Pure EMI (Principal + Interest only)

Banks ask for a one-time Processing fee (0.5% to 1% of the loan amount) plus GST on that fee. This is an upfront cost, not part of the monthly instalment.

Q: Is this calculator accurate for SBI, HDFC, and ICICI?

A: Yes. Math is universal.

Whether you borrow from a PSU bank like State Bank of India or a private giant like HDFC or Axis, they all use exactly the same “Reducing Balance” formula which is powered by this tool. The only difference is the Interest Rate they offer you.

Conclusion: You Are in Control

A loan is just a tool. Like a power saw — used properly it can be an asset for you. However, with bad technique, it can cut off your financial future. What lies between building wealth and drowning in debt is not luck—rather it’s mathematics.

CalcSahayak is here to ensure the math is always on your side. I am always with you to make you understand what you are signing for. After reading this whole article, I am confident – you now understand better than 90% of people who went and sign for something they don’t understand.

So, go ahead. Scroll back up. Move those sliders. Test different scenarios. Find the plan that lets you sleep peacefully at night.

Ready to start? Go to Calculator Top

A NOTE FROM THE DEVELOPER

Anusuya Ghosal Chatterjee

I am an independent developer and analyst passionate about transparency. I believe that making big financial decisions shouldn’t require a degree in mathematics.

I built the CalcSahayak EMI Calculator with a single mission: to bridge the gap between complex banking formulas and your daily budget. My goal is to provide a precise, easy-to-use tool that empowers you to plan your financial future with absolute clarity and confidence.

Disclaimer & Partner Disclosure: CalcSahayak provided this tool for educational content to help users estimate EMIs and plan budgets. Actual loan terms depend on the bank/NBFC, borrower profile, credit score, and regulatory changes. Always confirm exact figures with your lender and read the loan agreement carefully before signing.